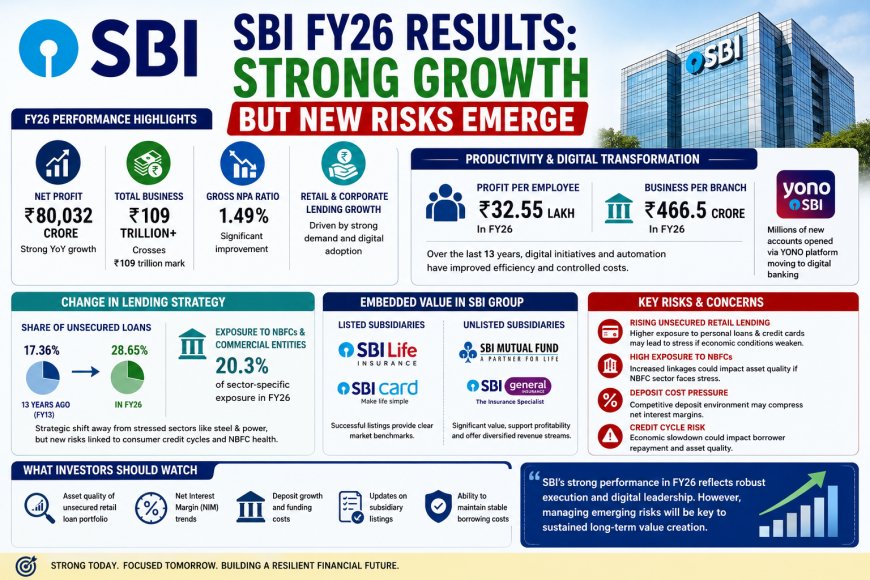

SBI FY26 Results: Strong Growth but New Risks Emerge

SBI reported ₹80,032 crore profit in FY26 with lower NPAs and strong business growth. Explore key risks, digital transformation, and future outlook.

Ellofacts

Ellofacts

SBI's FY26 Growth Story: Strong Performance Brings New Challenges and Opportunities

India's largest public sector lender, State Bank of India (SBI), delivered an impressive financial performance in FY26, reporting a net profit of ₹80,032 crore and crossing the ₹109 trillion total business milestone. The bank's continued focus on digital transformation, operational efficiency, and diversified lending has strengthened its position in the Indian banking sector.

However, despite these achievements, analysts and investors are closely monitoring emerging risks related to unsecured lending, NBFC exposure, and profitability pressures in a competitive banking environment.

SBI Posts Record FY26 Performance

SBI ended FY26 on a strong note with substantial growth across key financial parameters.

Key Highlights

-

Net Profit: ₹80,032 crore

-

Total Business: Over ₹109 trillion

-

Gross NPA Ratio: Reduced to 1.49%

-

Improved retail and corporate loan growth

-

Continued expansion of digital banking services

The sharp decline in non-performing assets (NPAs) reflects the bank's improved asset quality and disciplined credit management practices over recent years.

Digital Transformation Driving Efficiency

One of the biggest contributors to SBI's growth has been its aggressive digital banking strategy.

The bank's flagship digital platform, YONO, continues to attract millions of customers and has become a major channel for account openings, loan applications, and financial transactions.

Productivity Improvements

Over the past 13 years, SBI has significantly improved operational efficiency:

-

Profit per Employee: Increased to ₹32.55 lakh

-

Business per Branch: Reached ₹466.5 crore

These figures highlight how technology and automation have enabled the bank to serve a larger customer base while controlling operational costs.

Major Shift in Lending Strategy

SBI's loan portfolio has undergone a significant transformation in recent years.

Historically, the bank carried substantial exposure to sectors such as steel and power, which experienced stress during previous economic cycles. To reduce concentration risk, SBI has diversified its lending strategy.

Growing Share of Unsecured Loans

The share of unsecured loans has increased substantially:

-

FY13: 17.36%

-

FY26: 28.65%

This category includes:

-

Personal loans

-

Credit card loans

-

Consumer finance products

These products typically offer higher margins but also carry greater default risk during economic slowdowns.

Rising Exposure to NBFCs

SBI's exposure to Non-Banking Financial Companies (NBFCs) and commercial entities has also increased.

Sector-specific exposure to NBFCs now stands at approximately 20.3%, reflecting the growing interconnectedness of India's financial ecosystem.

While this strategy supports business growth and lending expansion, it also increases sensitivity to stress within the NBFC sector.

Hidden Value in SBI's Subsidiaries

Investors increasingly view SBI as a diversified financial services group rather than just a commercial bank.

Several SBI subsidiaries have already unlocked value through public listings:

-

SBI Life Insurance

-

SBI Cards and Payment Services

However, substantial value remains in unlisted businesses such as:

-

SBI Mutual Fund

-

SBI General Insurance

These businesses provide additional revenue streams and help reduce dependence on traditional lending income.

Key Risks Investors Should Monitor

Despite strong financial performance, several challenges remain.

1. Unsecured Retail Lending Risk

Regulators have repeatedly highlighted concerns about rapid growth in unsecured consumer credit.

If economic conditions weaken, personal loan and credit card defaults could rise, impacting profitability.

2. NBFC Sector Exposure

A slowdown in the NBFC sector could affect asset quality and repayment performance, creating pressure on the bank's earnings.

3. Deposit Cost Pressure

Competition among banks for deposits remains intense.

Higher interest rates offered to attract depositors may:

-

Increase funding costs

-

Compress net interest margins (NIMs)

-

Impact future profitability

4. Credit Cycle Risks

While current asset quality remains strong, changing economic conditions could alter borrower repayment behaviour and increase credit costs.

What Should Investors Watch Going Forward?

Investors should focus on several important indicators in the coming quarters:

-

Growth and quality of unsecured loan portfolios

-

Net Interest Margin (NIM) trends

-

Deposit growth and funding costs

-

Asset quality performance

-

Regulatory developments

-

Potential listing of SBI Mutual Fund and SBI General Insurance

These factors will play a crucial role in determining SBI's long-term growth trajectory and shareholder returns.

Conclusion

SBI's FY26 performance demonstrates the success of its digital transformation, operational efficiency, and diversified lending strategy. Record profits, improved asset quality, and strong business growth highlight the bank's financial strength.

However, rising exposure to unsecured loans and NBFCs introduces new challenges that investors cannot ignore. As the banking sector evolves, SBI's ability to balance growth with risk management will be critical in sustaining its leadership position and creating long-term value for shareholders.