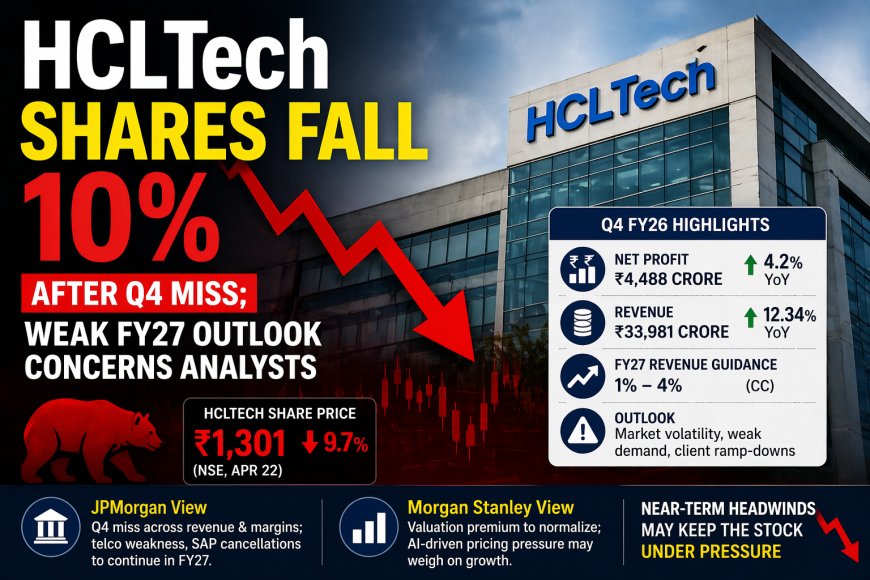

HCLTech Shares Fall 10% After Q4 Miss; Weak FY27 Outlook Concerns Analysts

HCL Technologies shares fell nearly 10% after Q4 results miss and weak FY27 guidance of 1–4%, raising concerns over demand and margins.

Ellofacts

Ellofacts

HCLTech Shares Drop Nearly 10% After Q4 Miss; Weak FY27 Guidance Worries Analysts

HCL Technologies saw its shares fall करीब 10% on April 22 after reporting weaker-than-expected Q4 FY26 results and issuing cautious revenue guidance for FY27.

The stock dropped as much as 9.7% to ₹1,301 on the NSE following the announcement.

Q4 Performance Highlights

For the January–March quarter, HCLTech reported a 4.2% year-on-year rise in net profit to ₹4,488 crore, compared to ₹4,307 crore in the same period last year.

Revenue from operations increased 12.34% YoY to ₹33,981 crore.

On a sequential basis, profit grew 10.1%, while revenue saw a marginal rise of 0.32%.

FY26 Annual Performance

For the full financial year FY26:

-

Net profit declined 4.3% to ₹16,642 crore

-

Revenue rose 11.18% to ₹1,30,144 crore

FY27 Guidance Remains Conservative

The company expects 1% to 4% revenue growth in constant currency for FY27. This cautious outlook reflects:

-

Ongoing market volatility

-

Reduced discretionary IT spending

-

Client-specific ramp-downs

CEO Commentary on Demand and AI

CEO C. Vijayakumar described the year as challenging due to an uncertain demand environment.

He highlighted that delays in client decision-making and reduced discretionary spending impacted performance. However, the company’s AI-led services are gaining traction, with annualised AI revenue crossing $620 million.

Management noted that AI is causing 2–3% pricing deflation in traditional deals, but increasing deal volumes are helping offset the impact.

Segment and Geographic Performance

-

IT & Business Services: +4.3% YoY

-

Engineering & R&D: +3.8% YoY

-

Software segment: -14.1% YoY

Region-wise:

-

India: +5.3%

-

Americas: +4.9%

-

Europe: -2.9%

Deal Wins and Hiring

HCLTech reported strong deal momentum with:

-

Q4 deal wins (TCV): $1.93 billion

-

FY26 total deal wins: $9.32 billion

Headcount increased by 802 employees in Q4, taking the total workforce to 227,181. The company added over 11,700 freshers during FY26.

Analyst Views

Analysts remain cautious on the stock due to weak demand signals and margin pressures.

-

JPMorgan Chase noted that the company missed estimates across revenue and margins, citing telecom sector weakness and SAP-related cancellations.

-

Morgan Stanley expects valuation premiums to normalise, highlighting macro uncertainty and AI-led pricing pressures.

Outlook

While AI-driven services present long-term growth opportunities, near-term challenges such as weak discretionary spending, pricing pressure, and global uncertainty may keep the stock under pressure.